Ensuring the security and quality of electricity supply across the GB transmission system is a huge challenge. The responsibility for this sits with National Grid by virtue of its Transmission Licence (granted pursuant to the Electricity Act 1989) and a series of codes, including the Balancing and Settlement Code (BSC). An obligation to comply with balancing requirements is also included in individual generation and supply licences.

In recent times the Capacity Market – introduced as one of the flagship components of Electricity Market Reform – has increased public awareness of market mechanisms for ensuring we have enough available capacity to ‘keep the lights on’. However, the full toolkit available to National Grid to balance the network remains, for many, relatively poorly understood. This article seeks to give a high-level overview of the different mechanisms used by National Grid. It also highlights some of the opportunities available to both energy and non-energy businesses to participate in and benefit from those processes.

BACKGROUND

The Capacity Market

The stated aim of the Capacity Market, introduced under the Electricity Capacity Regulations 2014 and Capacity Market Rules 2014, is to encourage investment in the replacement of older power stations and the provision of backup for more intermittent and inflexible low carbon generation sources. It also aims to support the development of more active demand management in the electricity market. It is the macro tool for ensuring there is sufficient capacity in the market generally to meet electricity demand in the future.

The Capacity Market works by National Grid estimating how much capacity is likely to be needed four years ahead. Electricity providers bid into a capacity auction, undertaking to provide electricity when needed if they win a contract. Successful bidders receive a steady payment at the successful price bid, as well as payments for electricity they sell. The price received by each successful participant is the marginal price bid which enables the required capacity to be contracted.

Auctions are repeated each year, four years in advance of when the electricity is required to be delivered, with smaller top-up auctions held one year before delivery for fine-tuning of contracted capacity levels. 2018/19 is the first year the Capacity Market will be running, hence the first auction at the end of 2014. The next auction, for capacity to be delivered in 2019/20, will be held in December 2015.

The secretary of state declared the results of the first auction as ‘fantastic news for bill-payers and businesses’ on the basis that the auction was ‘guaranteeing security at the lowest cost for consumers’. However, although the level of competition drove the costs of securing c.49GW of capacity way below expected levels, from a predicted price of over £70/kWh to a clearing price of £19.40/kWh, there are many who have questioned whether the auction in fact delivered on its stated aims.

The auction price went too low to attract a significant level of investment in new power stations. Only one large new power station (the c.1600MW gas-fired plant at Trafford, Manchester) secured a contract. Also, less than 1% of the capacity secured came from demand-side response firms. Helping to fund the refurbishment of existing coal-fired generation has, arguably, allowed our most carbon-intensive generating stations to remain operational for longer – perhaps tough to reconcile with the aims of the competing policy initiative of the carbon price floor.

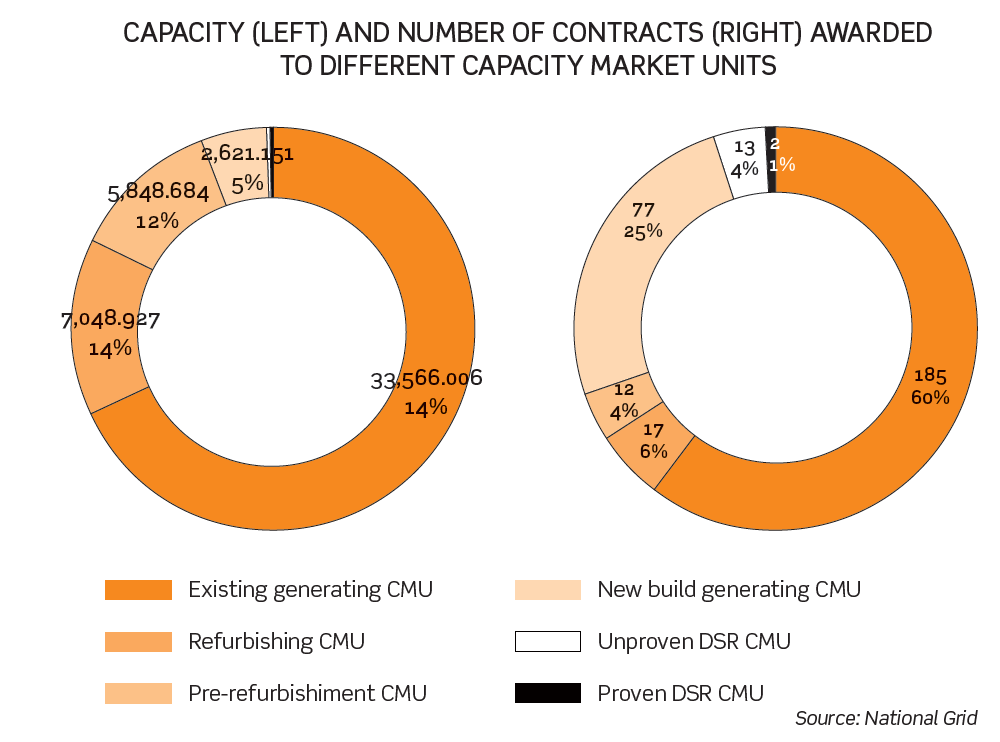

The diagram below illustrates the capacity (left) and number of contracts (right) awarded to different Capacity Market units (CMUs) under the first auction round, split by type of participant.

While the Capacity Market is intended to go a long way towards ensuring sufficient generating capacity for the future, it is not sufficiently sophisticated to manage the real time balance between system demand and total network generation. This is, instead, managed by National Grid through the balancing mechanism and, in advance of this, by power exchange trades, forward energy trades and the use of energy balancing contracts.

The balancing mechanism

Under the balancing mechanism, electricity suppliers and generators contract with each other (and provide details of this to National Grid, through the BSC company, Elexon) one hour before each half-hourly ‘settlement period’. They also provide estimates of their likely actual generation and demand levels and what they would charge or be prepared to pay for altering those levels (known as ‘bids and offers’).

Each generator and supplier is charged by Elexon, for any imbalances between their actual and notified position which contribute to an overall transmission system imbalance. These ‘cash out’ charges are designed to incentivise generators and suppliers to balance their own positions in the market ahead of the settlement period.

While potential system imbalances leading up to the balancing mechanism are inevitable, National Grid tries to minimise these in advance of the balancing mechanism by procuring balancing services. The following is a brief overview of some of the key contractual balancing services procured in advance by National Grid.

RESERVE POWER SERVICES

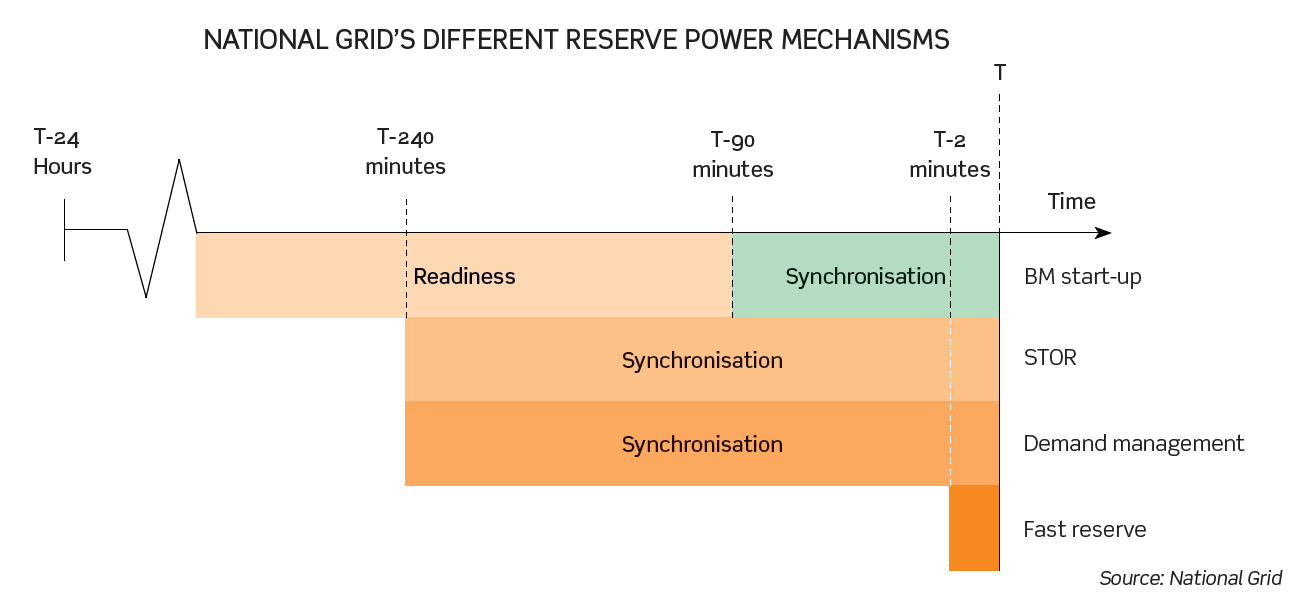

National Grid needs access to sources of ‘reserve’ – either generation or demand reduction – to be able to deal with unforeseen demand increase and/or generation unavailability. Different contracted sources can be called upon ahead of the relevant settlement period(s) to enable National Grid to select the most suitable (and cost-effective) source based on the nature of the imbalance. The main variable in the types of reserve contracted is the length of time it takes for that reserve to be delivered after instruction. The different mechanisms at National Grid’s disposal are illustrated in the diagram below and summarised in the sections that follow.

Short term operating reserve (STOR)

STOR allows National Grid access to reserve in the form of either generation or demand reduction and is procured via competitive tender. There are normally three tender rounds per year. All the interested parties have to pre-qualify before the tender and sign a framework agreement.

A STOR provider must be able to:

- offer a minimum of 3MW or more of generation or steady demand reduction (this can be from more than one site);

- deliver full MW within 240 minutes or less from receiving instructions from National Grid; and

- provide full MW for at least 2 hours when instructed.

National Grid makes two forms of payment as part of the service. Availability payments are made in return for service providers making their unit available for the STOR service within an ‘availability window’, and utilisation payments are made where service providers actually deliver energy on instruction.

Over the last few years (due, in part, to the anticipated introduction of long-term contracts under the Capacity Market), the length of STOR contracts has reduced significantly. While, in years gone by, 13-year contracts were available, the norm is now for these to be of less than two years’ duration. This has made it more challenging for standby generating plants to secure long-term project finance under STOR alone, due to greater uncertainty of revenues.

Demand-side balancing reserve (DSBR)

DSBR is targeted at commercial and industrial energy consumers that can agree to reduce demand between 4pm and 8pm on winter weekday evenings (when electricity demand is typically highest) in return for a payment. This reduction can be achieved in a number of ways, such as by running on a backup on-site generation rather than using electricity from the grid.

DSBR is contracted through tenders in a similar way to STOR although, as with STOR, can either be contracted directly with National Grid or through a growing number of aggregators. Payments are made for both capability and for demand reduction that is actually delivered.

Fast reserve

Fast reserve involves the rapid delivery of power following receipt of an electronic despatch instruction from National Grid, through either increased output from generation or reduction in consumption from demand sources.

As with STOR, fast reserve is procured via a monthly tender process and requires pre-qualification and the entering into of a framework agreement in advance of tendering. Successful participants receive an availability fee for each hour in a prescribed period where the service is available and a utilisation fee for the energy delivered. The provider may also be entitled to a holding fee.

To be eligible, the provider must be capable of delivering active power within two minutes of the despatch instruction at a delivery rate in excess of 25MW/minute, and the reserve energy must be sustainable for a minimum of 15 minutes. The provider must also be able to deliver a minimum of 50MW, meaning the number of potential participants is much smaller than with STOR or DSBR.

BM start-up and hot standby

BM start-up service is used by National Grid to ensure that sufficient generating capacity is in a state of readiness to meet anticipated demand plus an adequate operating margin, on a day-ahead basis. The service gives National Grid access to generation units which would not otherwise have run, and which, because of their technical characteristics, require longer lead times to ‘warm up’ and deliver electricity at the required level.

Participating generators must have the ability to prepare the generator towards a state of readiness (BM start-up) in order to deliver the required power within 89 minutes from instruction. They must also be capable of terminating the process at any time prior to reaching hot standby – the name given to an actual state of readiness to deliver power to the system within 89 minutes of instruction.

The BM start-up service is procured through bilateral agreements between National Grid and generators, which set out the specific services and costs. The BM start-up rates paid reward the generator for making a unit available for despatch. A separate hot standby payment is made to cover the cost of sustaining a state of readiness for the required period.

Supplemental balancing reserve (SBR)

SBR aims to keep power stations in reserve that would otherwise be closed or mothballed. This acts as a safety net in the event of there being insufficient capacity available in the market to meet demand.

FREQUENCY RESPONSE SERVICES

National Grid has a licence obligation to control frequency within specified limits (±1% of nominal system frequency (50.00Hz) save in abnormal or exceptional circumstances). National Grid must, therefore, ensure that sufficient generation and/or demand is on standby to manage potential frequency variations.

System frequency is a continuously changing variable that is determined and controlled by the second-by-second (real time) balance between system demand and total generation. If demand is greater than generation, the frequency falls and vice versa. As more intermittent energy generation such as wind and solar is added to the network, the risk of rapid frequency changes will increase the challenge of managing frequency levels.

The toolkit available to National Grid to manage frequency includes the following mechanisms.

Mandatory frequency response (MFR)

All generators who are connected to the GB transmission system (and therefore subject to the BSC) must have capability to provide MFR – an automatic change in active power output. A service provider will receive a holding payment (for being capable of delivering when called into frequency response mode) and a response energy payment (for the amount of energy delivered).

Firm frequency response (FFR)

FFR is open to a much wider range of participants than MFR, with the services procured through a monthly competitive tender process. Pre-qualification and the signature of a framework agreement are pre-requisites to participation in the tender. Tenders can be for low and/or high frequency events. The technical qualifying criteria to be eligible for an FFR contract include the delivery of a minimum of 10MW of response energy. The payment structure is set out in the Connection and Use of System Code and includes payments for availability, nomination fees and fees for the actual response energy delivered.

Frequency control by demand management (FCDM)

FCDM provides frequency response through automatic interruption of demand customers when the system frequency falls below a certain level. Participating customers must be able to reduce demand within two seconds of instruction, for a minimum of 30 minutes and at least 3MW must be delivered.

This service is provided through bespoke bilateral negotiations with providers. Once the relevant tripping equipment has been installed and tested, a site can join the scheme subject to signing an FCDM ancillary service agreement. Once a provider has agreed terms they are required to declare availability for each settlement period on a weekly basis. National Grid then decides whether to accept this availability and, if accepted, an availability fee is paid.

FFR and FCDM may be financially attractive propositions for many businesses which are able to interrupt their demand for short periods of time. While the minimum threshold for participation can be prohibitive for businesses to participate with National Grid directly, the increasing role of demand response aggregators may help businesses to realise revenues through these mechanisms.

OTHER SYSTEM SECURITY MEASURES

There are several other tools at National Grid’s disposal to aid system security. In summary, these are:

- Transmission constraint management: this is required where congestion is preventing the transmission system from transmitting power supplied to the demand location. National Grid enters into bilateral contracts on an ad hoc basis with service providers to increase and/or decrease the amount of electricity at different locations on the network, mostly commonly through agreeing a cap or collar on the output of a power station. The structure of the payments received by the service provider will be determined by the style of the constraint management contract.

- Maximum generation service: access to capacity which is outside the generator’s normal operating range is initiated in specific emergency circumstances by the issuing of an emergency instruction in accordance with the BSC. This service is provided on a non-firm basis through long-term commercial service agreements, with providers being paid for any energy that they deliver.

- Intertrips: these are automatic control arrangements where generation or demand may be reduced or disconnected from the transmission system following a system fault event to relieve localised network overloads, maintain system stability, manage system voltages and/or ensure quick restoration of the transmission system.

- Black start: This is the procedure to recover from a total or partial shutdown of the transmission system which has caused an extensive loss of supplies, and entails isolated power stations being started individually and gradually reconnected to each other to form an interconnected system again. Black start capability is usually a consideration when the plant is being built and is procured on a bilateral basis. Providers are paid an agreed fee per settlement period for their availability as well as utilisation payments if used.

OPPORTUNITIES

The balancing market is certainly big business, with the total cost of balancing services amounting to c.£1bn in 2013/14. The cost of the Capacity Market in future years will also be significant. As patterns of electricity usage, generation and transmission change over the coming years, the challenges of balancing the network to meet the needs of consumers will also evolve. Technology advances – and in particular the role of energy storage within the network – are likely to play a significant role in the development of balancing services. The pressures of carbon abatement and the inevitable increasing role of demand response (assisted by aggregators bringing such capability to the market) are also likely to increase the participation in balancing services of high energy consumers, as more become aware of the potential for capitalising on this potential revenue stream.

By James Phillips, partner, Burges Salmon LLP.

E-mail: james.phillips@burges-salmon.com