The revised Energy Bill was published on 29 November 2012 after extensive consultation following publication of the government’s electricity market reform (EMR) proposals in December 2010. The Bill will push through fundamental reforms to the UK electricity market that will affect the entire sector in one shape or form.

The government’s proposed reforms aim to provide investors with transparency, longevity and certainty to attract further investment in low-carbon energy (the government estimates that as much as £110bn is required before 2020) while safeguarding security of supply and customer affordability. This year will be crucial for further development of the EMR proposals, as a number of elements will be consulted on and clarified.

The key elements of the EMR proposals are:

- feed-in tariffs with contracts for difference (CfDs) – a new incentive for the development of renewable generation (>5MW), as well as supporting new nuclear power projects and carbon capture and storage (CCS);

- capacity market – a mechanism to support security of supply, if needed;

- access to markets – powers to ensure long-term power purchase agreements (PPAs) are available to independent generators and measures to improve the liquidity of the electricity market; and

- emissions performance standard (EPS) – to limit the carbon dioxide emissions permitted from new fossil fuel-powered generating stations.

This article primarily focuses on feed-in tariffs with CfDs but will also discuss the other EMR proposals mentioned above.

FEED-IN TARIFFS WITH CFDS

CfDs will replace the Renewables Obligation (RO) as the main financial subsidy for the development of renewable projects over 5MW, operating alongside the existing feed-in tariff regime that will continue to support small-scale (<5MW) renewable generation. It will also encourage new nuclear and CCS projects. The Energy Bill contains provisions for the secretary of state (SoS) to implement CfDs through secondary legislation. CfDs are long-term contracts allocated to eligible generators and funded by contributions from licensed electricity suppliers to provide stable and predictable incentives. A new government-owned company will act as the single CfD counterparty.

Setting the strike price

The fundamental basis of the CfD model is the provision of a pre-identified ‘strike price’ to the generator for all eligible electricity generation. This strike price will operate against a reference wholesale market price – if the reference price is lower than the strike price, the generator will be paid the difference between the two prices, whereas if the reference price is higher than the strike price the generator will have to pay back the difference1.

For renewables projects, the strike price will initially be set unilaterally by the government and will vary for different technologies. Renewables strike prices for the period 2014-19 will be issued and consulted on in the draft delivery plan to be published in July 2013, and will be finalised and published in the first five-yearly EMR delivery plan due in Q4 2013. Thereafter, prices will be updated annually, with the government’s ultimate aim being to switch to competitive price-setting. Further information on the strike price setting process for nuclear and CCS will be published in July 2013 after the government’s CCS funding competition closes.

By providing a fixed strike price, the government is seeking to ensure that generators receive a predictable, inflation-linked payment for electricity generation, thereby removing uncertainty arising from wholesale price volatility2.

A common misunderstanding is that the strike price is the guaranteed revenue a generator will receive. This is not the case since the CfD payment relates to the gap between the reference price and the strike price, meaning the generator takes the risk of not being able to find a route to market for its power at the reference price.

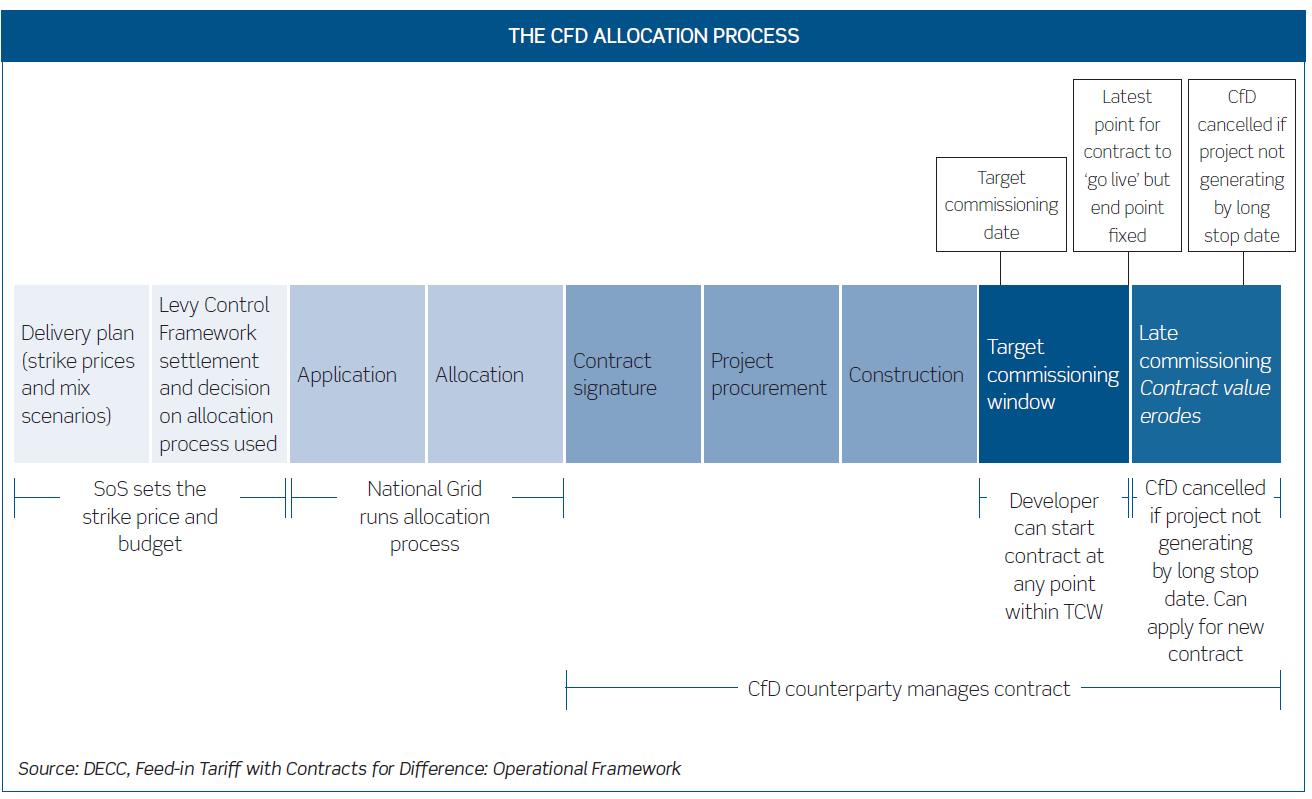

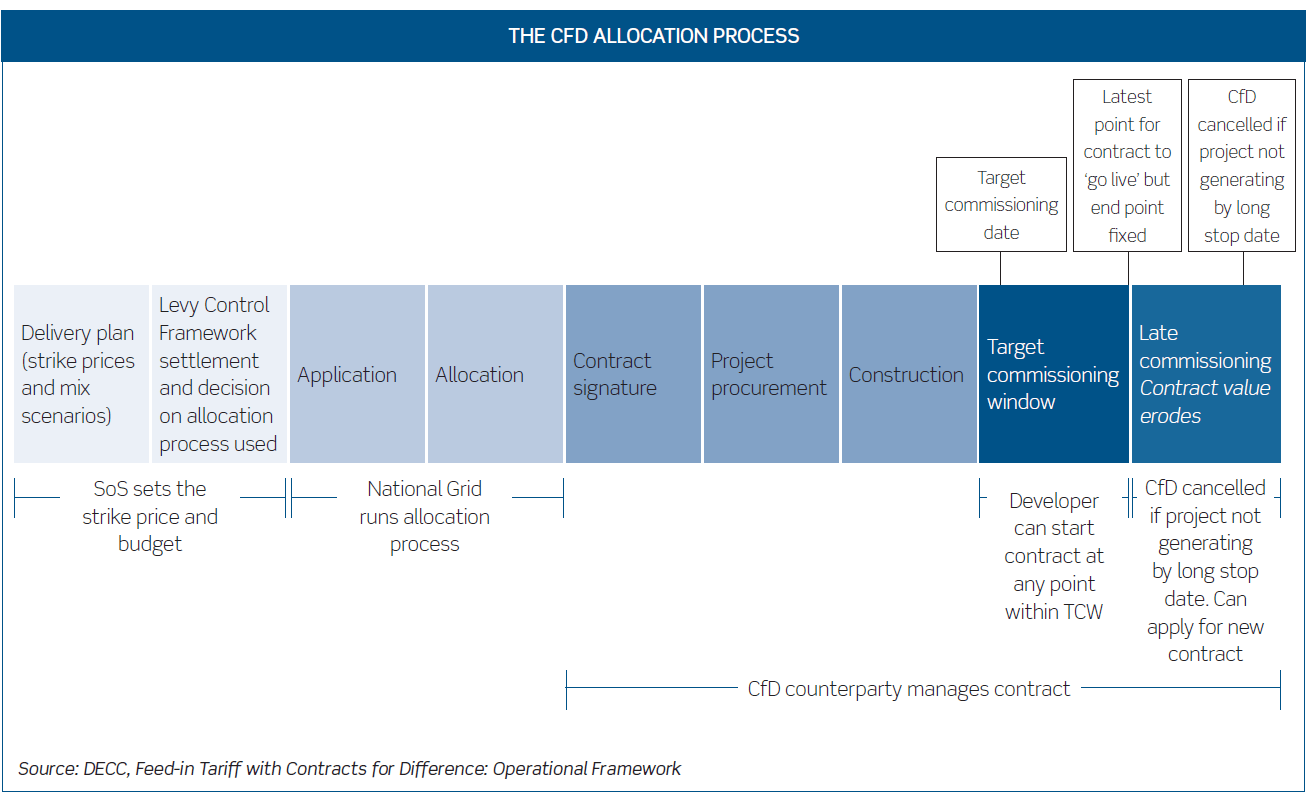

Allocation and eligibility of CfDs

Developers wishing to apply for CfDs will have to satisfy National Grid, the appointed ‘system operator’, as to the following:

- Eligibility – the proposed project is from an eligible technology3.

- Achievement of a specified stage in the development process – this will be prescribed for each individual technology. For example, wind projects will require proof of planning permission and an accepted network connection offer.

- Capacity of the proposed facility – a generator will only be able to claim CfD support for its contracted capacity. Generators will have to apply for additional CfDs to cover any additional capacity.

- Target commissioning date.

Initially, CfDs will be allocated on a first-come, first-served basis. The system operator will run the application system and determine an applicant’s eligibility. When satisfied, it will instruct the CfD counterparty to enter into a CfD on prescribed parameters.

Once a certain amount of the government’s CfD ‘budget’ has been allocated (which the government has suggested could be 50% of the budget for each delivery year), six-monthly technology-specific allocation rounds are proposed to be adopted. These rounds will allocate CfDs on the basis of objective criteria (to be confirmed) if there is more demand than available resource. The government envisages that this could happen as early as 2017, with movement to technology-neutral auction processes in the 2020s, by which time the government hopes that all low-carbon technologies will be able to compete on an equal footing.

The majority of renewable energy technologies will be funded from one central budget (referred to as the ‘general pot’). However, certain technologies capable of particularly rapid deployment (biomass conversion and solar) will only be able to receive funding from a separate ring-fenced budget.

The CfD contract

A CfD will be a bilateral private law contract between the generator and the CfD counterparty under which payments will flow between the parties for a term of 15 years for all renewables (the contract term for nuclear and CCS is undetermined). The RO currently provides support for 20 years and the industry is likely to press the government as to why it has opted for this reduction, a key concern being that it may deter investors seeking long-term returns, such as pension funds.

A detailed draft CfD heads of terms was published alongside the Bill and is expected to be finalised in July 20134. CfDs will be standardised across technologies, subject to variations required for operational differences, eg intermittent or baseload power.

Previously, one of the key concerns with the government’s proposals for allocating CfDs was a requirement for developers to reach ‘financial close’ before entering into a CfD. This condition has now been removed and developers will be able to apply for a CfD once the eligibility criteria have been satisfied (see above) and subject to developers demonstrating a ‘substantive financial commitment’ to the project within a designated timeframe from CfD execution. If this milestone is not met, the CfD can be terminated – thereby allowing the budget to be reallocated. The government has not confirmed what will constitute a ‘substantive financial commitment’ (eg a minimum spend amount or confirmation of an irrevocable financial investment decision having been made) but has suggested that the milestone deadline will be one year from entry into the CfD. Developers will therefore have to balance the benefit of an early CfD application against the risk of termination if financial commitment is delayed.

Once a CfD has been allocated, the project must be commissioned within a ‘target commissioning window’ (TCW), which is based on the target commissioning date provided by the developer during the application process. Generators that commission after the end of the TCW will still benefit from the contracted strike price, but the CfD term will be reduced to reflect the delay in commissioning. Failure to meet an ultimate commissioning long stop date will result in termination of the CfD.

Payments

The draft Energy Bill empowers the SoS to require electricity suppliers to make payments to the CfD counterparty (the ‘supplier obligation’) so that it, in turn, can make payments under CfDs. The CfD counterparty, or potentially a settlement agent, will administer the flow of monies from electricity suppliers to generators and vice versa on what is anticipated to be a monthly basis. The CfD counterparty’s payment obligation will be conditional on it having received payments from electricity suppliers and, thus, the generator will bear the risk of suppliers not paying or delaying payment under the supplier obligation. One suggestion made to counter this risk is for the CfD counterparty to be provided with a working capital cushion to cater for any mismatches in flows. It remains to be seen whether the government will concede this.

Future changes in law and force majeure

The draft CfD heads of terms confirms that generators will be provided with protection against certain changes in law and regulation, although not from ‘general’ changes in law that apply across the economy or the energy sector as a whole. Any compensation payable by the CfD counterparty for a change in law will be paid through an adjustment to the strike price rather than a lump sum payment. The change in law provisions are two-way so that any change in law benefiting generators may cause the strike price to be adjusted down accordingly. The provisions are being looked at carefully, and with an element of suspicion by developers, to assess the scope for government to negotiate the strike price downwards during the term.

The force majeure provisions contained within the draft heads of terms are relatively limited in scope and do not, for example, protect a generator where it is unable to meet the relevant project milestones (including securing substantive financial commitment) as a result of circumstances outside its control.

INVESTMENT CONTRACTS

While the Energy Bill sets out the framework for the policy measures being introduced, the details of each policy (including the CfD operational provisions) will be contained in secondary legislation that is unlikely to be finalised until 2014. As an interim measure, the government will allow developers to make final investment decisions ahead of full EMR implementation by way of ‘investment contracts’ granted as part of the government’s final investment decision (FID) enabling process. Investment contracts will be early form CfDs entered into between the SoS and developers that will be transferred to the CfD counterparty once established.

THE DEMISE OF THE RO AND THE FUTURE OF ROCS

The RO is currently the main source of financial support available for renewable energy projects and places an obligation on suppliers to source a certain proportion of the electricity they supply from renewable sources. Suppliers can comply with this obligation by surrendering Renewables Obligation Certificates (ROCs, the tradeable certificate evidencing renewable generation issued to generators) or by paying a penalty (referred to as the buy-out price).

The RO will close to new projects from 31 March 2017. RO-accredited projects will be ‘vintaged’ after this date but will still receive a full 20 years of support (subject to the ultimate 2037 RO end date). There will be some very limited flexibility around the RO closure date for projects delayed for reasons beyond their own control, such as delays in grid connection or caused by radar issues.

Renewable generation that is already accredited under the RO will not be eligible to transfer to the new CfD regime, while those projects seeking accreditation between 2014 and 2017 will be required to make a one-off election between the two schemes.

Concern has been voiced by the renewables sector as to how the value of ROCs will be maintained, as current legislation only covers maintenance of ROC values and obligations on suppliers to procure ROCs until 2027. To provide comfort to RO projects after this date, the government has confirmed that the RO will be replaced with a certificate purchase obligation under which Ofgem will be required to purchase ROCs using proceeds raised from a levy imposed on electricity suppliers. Previous policy documentation had suggested that the redemption value of ROCs under the certificate purchase obligation would be the 2027 buyout price plus 10% additional headroom. However, the draft Bill leaves this to be determined in subsequent secondary legislation.

The government plans to consult on the arrangements for the RO transitional period in March 2013.

MARKET LIQUIDITY AND ACCESS

The government acknowledges that investment by independent developers is currently hindered by a lack of market liquidity. Although the government has recognised that the industry (together with Ofgem) is best placed to deliver improvements, the Energy Bill contains powers to enable the SoS to modify supplier licence conditions to improve wholesale electricity market liquidity, if necessary, in the future. The Bill also contains powers to modify supply licences for the purposes of reducing barriers to entry associated with the power purchase agreement (PPA) market, again, if necessary.

OTHER IMPORTANT ASPECTS OF ELECTRICITY MARKET REFORM

In addition to the CfD model outlined above, the EMR proposals include a number of other key components:

- An emissions performance standard (EPS), which sets a regulatory backstop on the amount of carbon that can be emitted from new fossil fuel generating stations. This will initially be set at 450g CO2/kWh – a level that will ensure that any new coal-fired power stations will have to fit CCS to be lawfully operational. This is anticipated to help further encourage low-carbon generation since the EPS concept will inevitably push up costs for fossil fuel generation.

- A capacity market, allowing for capacity auctions (not open to low-carbon plants with CfDs) from 2014 for delivery of electricity generating capacity in the winter of 2018-19 (and onwards). It is hoped that a capacity market will help ‘keep the lights on’ even at times of peak demand, thereby insuring against future supply shortages. The government is also consulting on the potential for using reductions in demand from large electricity consumers. The final detailed design proposals for the capacity market will be published by May 2013 and an estimate of the amount of capacity to be auctioned in 2014 will be published by the end of 2013.

- The carbon price floor, which was legislated for through the Finance Act 2011 and will affect fossil-fuelled plants. It will be introduced from 1 April 2013 at around £15.70/tCO2 and follows a straight line to £30/tCO2 in 2020, rising to £70/tCO2 in 2030 (real 2009 prices). It aims to provide long-term certainty about the cost of carbon in the UK electricity generation sector, and send clear pricing signals towards low-carbon generation. The government’s long-term desire is to have a wholesale electricity price that reflects the cost of carbon and allows generators to compete equally without the need for intervention.

- Powers for the government to set a decarbonisation target for the power sector for 2030. The inclusion of an actual decarbonisation target in the Bill itself has been a key area of contention within the coalition government. Although the government is currently intending to delay any target setting decision until 2016 (after the Climate Change Committee has provided advice on the fifth Carbon Budget covering the corresponding period), this stance is likely to generate much debate during the House of Commons’ review.

CONCLUSION

A number of changes have been made to the Energy Bill since its initial publication in May 2012 for pre-legislative scrutiny. These changes will be welcomed by the low carbon sector, as will the fact that the government is clearly investing significant time in the development of the CfD mechanism as evidenced by the detailed draft heads of terms. However, clarification of the finer details of the proposals will only become apparent during the course of various consultations planned for 2013 and following the publication of the relevant secondary legislation needed to flesh out the framework for reform provided by the Energy Bill.

The government’s EMR proposals, when enacted through the Energy Bill and accompanying secondary legislation, will bring about the most fundamental change to the UK electricity market since privatisation. Although this article has focused on the impact of CfDs on low-carbon generation, the proposals will affect all types of generation, including the gas sector. Indeed, the gas sector will also find some encouragement in recent policy developments, such as the potential benefits of the proposed capacity mechanism, grandfathering of EPS levels and the government’s recently published gas strategy. Many will be closely observing the debates that will inevitably follow in respect of the timing and content of a 2030 decarbonisation target, which may give a strong steer towards the likely composition of the UK’s energy mix over the coming years.

Notes

- The reference price for intermittent generation will be the hourly, day ahead ‘GB Zone’ price resulting from the EU market coupling arrangements scheduled for implementation in 2013. The government is conducting more analysis to determine the reference price for baseload generation but it will likely be drawn from the forward markets.

- The Consumer Price Index will be adopted as the inflation index for the CfD. However, it is not yet clear whether the strike price will be fully or partially indexed.

- The list of eligible technologies will be published in upcoming secondary legislation, but will include all technologies that are currently eligible for the renewables obligation together with CCS and nuclear.

- /in-house-lawyer/wp-content/uploads/sites/9/2013/02/7078-electricity-market-refrorm-annex-b-1.pdf.