When we ordinarily refer to compliance in goods and services tax (GST), what strikes our minds is the filing of GST returns and settling the GST due within the stipulated taxable period. It has been more than two years now since the implementation of GST in Malaysia. The compliance rate for GST filing thus far has been high, with an average rating of above 95%.

However, when it comes to the settlement of GST dues, the compliance rate is not as high as the GST filing rate. It has been reported that about one-third of the companies audited by the Royal Malaysian Customs Department (RMC) submitted incorrect returns by omitting information, understating output tax or overstating input tax. This kind of non-compliance undermines the government’s revenue, distorts competition as it gives the non-compliant business an advantage in the form of cash flow and compromises equity as this may encourage further non-compliance in other aspects of GST. This article aims to highlight the other aspects of compliance requirement under the GST Act 2014 and the sanctions that the RMC may impose in such circumstances.

Customs’ experience

GST, or Value Added Tax (VAT) as it is known in some countries, is regarded by economists as a fair and efficient tax system. It is a very effective tax as it places all businesses on a level playing field. The popularity of this tax is evident from its implementation in over 150 countries, with even the income tax-free Gulf countries planning to implement GST soon.6 In Malaysia, GST has been credited as having filled the government coffers during this challenging economic period, with a projection of RM42 billion in collection this year.

RMC’s recent experiences show that the non-compliance culture is prevalent among smaller businesses as this segment has a rate of 40% when it comes to errors in GST returns. This phenomenon is not peculiar in Malaysia as it is also prevalent in other advanced economies. Not only is there a prevalence of incorrect returns, RMC has also noticed that the non-compliance by small businesses commonly spans all spectrum of GST obligations. Some small businesses are completely outside the GST system, some only register to illicitly claim a refund; many have a poor record-keeping culture, which then leads to poor filing and payment compliance. This is compounded further by businesses that are ignorant of deadlines. Ninety-four per cent of the GST-registered persons in Malaysia are from the small and medium-size enterprise (SME) segment and inevitably, GST compliance cost is a challenge for many SMEs. Meeting their GST obligations means additional costs for them, especially in obtaining proper professional advice, employing competent finance staff and investing in reliable GST software and ensuring proper GST compliance return.

Why CBOS 3.0?

Some businesses regard that the compliance costs are high and, in some instances, even outweighs the net amount input credit remitted, which potentially leads to the failure to comply or register, thus allowing the vicious shadow economy to prosper. This needs to be addressed as tax laws and its implementation must be fair. This sense of awareness had led the RMC to recently launch the Customs Blue Ocean Strategy (CBOS) Operation 3.0. The objective of this operation is not merely to detect issues for further GST audit or investigation, but to also encourage taxpayers to comply with the law. The approach for this operation is “Informed Compliance” rather than “Enforced Compliance” with the aim of assisting taxpayers, especially SMEs. Informed compliance focuses on educating taxpayers by making friendly visits to traders to explain and assist them in complying with GST obligations and provides channels for taxpayers to share their grievances and enable them to provide feedback. The RMC conducts handholding programmes and consultation sessions to achieve this. On the other hand, the enforced compliance focuses on litigation where errant taxpayers will be prosecuted.

The core principle of the GST compliance model is to make compliance as easy as possible. Having said that, taxpayers found to be wilfully abusing or seeking to abuse the system will incur the wrath of the full force of the law. In this context, the ongoing CBOS operation has three levels:

(i) Verification;

(ii) 30 days to comply;

(iii) Enforcement action.

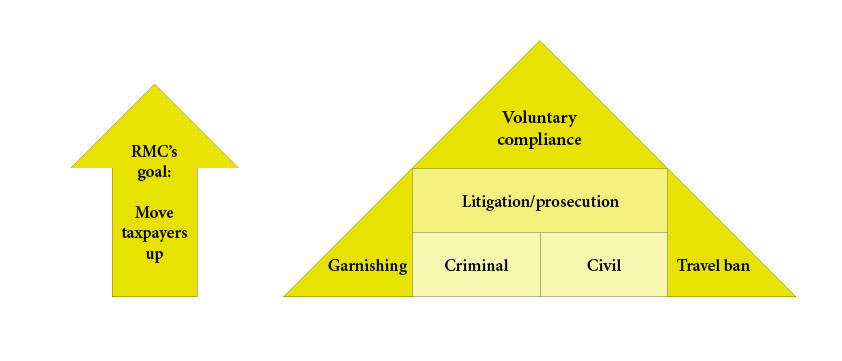

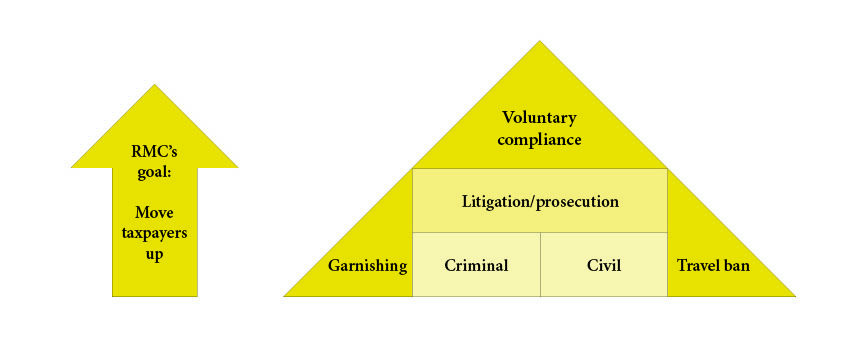

Via the verification exercise, the RMC will examine the GST treatment adopted by businesses and the corresponding business documentations. If any non-compliance is detected, then the affected taxpayer will be advised to amend the GST-03 return and settle the amount of GST due within 30 days. If the taxpayer fails to amend the GST-03 return and/or settle the amount due within 30 days, then a full GST audit will be conducted and enforcement actions such as prosecution, civil proceedings to recover the amount due, garnishing of assets, imposition of travel restriction and recovery proceedings against directors will be employed. Hence, the RMC encourages voluntary compliance with taxpayers coming forward to correct their previous mistakes. From the RMC’s past experience, voluntary compliance can only be encouraged when taxpayers are aware that non-compliance would be detected and sanctioned accordingly. Studies have shown that taxpayers’ behaviour is strongly linked to the GONE (Greed, Opportunity, Needs and Expectation of getting caught) theory. “Greed” refers to excessive desirous of wealth or profit; “Opportunity” refers to being in the right position to commit the offence; “Needs” refers to a condition in which something necessary is required or wanted; and, finally, the “Expectation” of getting caught refers to the degree of enforcement.

Below is the voluntary compliance model:

It is notable from past experiences that CBOS operations not only collect additional GST revenue from noncompliant taxpayers, but also lead to a higher declaration from taxpayers who are not audited.

Areas of risk detected in CBOS operation

Based on the RMC’s experience from previous CBOS operations, these are the key issues that are usually detected:

- Incorrect treatment of standard-rated supplies as zero-rated supplies

- Failure to account for GST on non-trade income and fixed asset disposals (sale or trade-in)

- Reimbursement/disbursement

- Deemed supplies, e.g. provision of gifts

- Fringe benefits

- Claiming of input tax on “blocked” expenses

- Incorrect use of GST codes

- Incorrect decisions in setting up codes e.g. zerorating based on billing address

- Incorrect entering of data

- Transposition or formula errors

- Failure to identify and take account of legislative or policy changes

- Poor communication of business changes (e.g. restructuring) to RMC audit team.

The above results in the RMC assessing each audit case on a case-to-case basis in evaluating the type of action and sanction to be taken. The common provisions of the GST Act 2014 usually applied by the RMC in charting its course of action are:

- Section 9

Determine whether there is a supply of goods or services in Malaysia, including deemed supply and any importation of goods into Malaysia. - Section 33

Ensure that a proper tax invoice is issued by all suppliers. - Section 36

Duty to keep full and true records in respect of all goods and services supplied, all goods imported and any other records required under the GST Act 2014. - Section 41

Furnishing return in the manner prescribed by law according to the time frame prescribed. - Section 88

Imposition of penalty for incorrect return which carries a fine not exceeding RM50,000, imprisonment not exceeding three years or both. There is also a penalty equal to the amount of GST undercharged. - Section 89

Imposition of penalty for GST evasion and fraud which carries for the first offence, a fine not less than 10 times and not more than 20 times of the GST amount evaded or defrauded, imprisonment not exceeding five years or both. For the second and subsequent offences, a fine not less than 20 times and not more than 40 times of the GST amount evaded or defrauded, imprisonment not exceeding seven years or both. - Section 90

Imposition of penalty for causing improper GST refund or entitlement to relief which carries a fine not exceeding RM50,000, imprisonment not exceeding three years or both. There is also a penalty equal to two times of the amount improperly refunded or entitled as a relief.Recovery mechanisms

Despite best efforts, there will be a segment of taxpayers who will continue to flaunt the law. While the RMC may not be able to immediately detect all non-compliant behaviours, sooner or later, with the concerted GST audit initiatives, taxpayers should act now before the long arm of the law catches up with them. The following are some recovery mechanisms that the RMC may apply on recalcitrant taxpayers:

(a) Offsetting unpaid tax against refund

In cases where a taxpayer has failed to pay any amount of GST due and payable, the Director General of the RMC may offset against the unpaid GST any amount GST refundable. The amount offset will be treated as payment or part payment for the GST due.

(b) Recovery of GST as a civil debt

Notwithstanding any appeal before the GST Appeal Tribunal, the Minister of Finance may recover the unpaid GST as a civil debt due to the government. In this type of proceedings, the production of a certificate signed by the Director General of the RMC of the sum due shall be conclusive evidence and authority for the court to give judgment for that amount.

(c) Seizure of goods for the recovery of tax

Any goods in excise control or customs control or at the taxpayer’s place of business may be seized until the GST due is settled. The Director General is also empowered to seize or sell any goods belonging to the person liable.

(d) Power to collect tax from person owing money to taxable person

In instances where GST is due, the Director General may, by notice in writing, require any person by whom any money is due, accruing or may become due and payable to a taxable person who owes the GST, to pay the said money which will be used to pay the GST due. This power can also be used on any person who holds or may subsequently hold money for or on account of the person who owes GST.

(e) Travel restriction

Where the Director General has reason to believe that a person is about or is likely to leave Malaysia without paying the GST due, that person can be prevented from leaving unless and until the sum owed is settled.

(f) Power to require security

For the due compliance of the law and protection of revenue, the Director General may require any person to give security for the payment of any GST which may become due and payable from him.

(g) Imported goods not to be released until tax paid

Any imported goods can be withheld in the customs control until the GST on those goods has been paid in full except.

(h) Liability of directors

In relation to a company that is being wound up, where any GST is due, the directors shall together with the company be jointly and severally liable for the sum due. The directors shall only be liable where the assets of the company are insufficient to meet the amount due.

Conclusion

Hence, it is essential that businesses invest in their workforce by ensuring their employees are provided regular training, which in return will enable the employees to familiarise themselves with the GST law and the updates. There should also be internal training or knowledge sharing sessions to enable the transfer of GST knowledge and awareness within the business.

Good training is hoped to result in good record-keeping culture. Businesses have been reminded on many occasions to maintain complete records and documents supporting GST documents. Transactions must also be recorded on a timely basis and GST worksheets/computations should be kept. This must be supplemented with a reliable accounting system that enables accurate.

Businesses must also adopt effective internal practices that allow the management to identify exceptional transactions and identify the appropriate GST treatment. It is good practice to implement a second level of review and a periodic review of the above.

As much as the RMC is committed via the Informed Compliance initiative to provide further assistance to businesses to ensure GST compliance, leniency will not be extended to GST evaders.16 An estimated RM3 billion in GST arrears will be collected from the CBOS 3.0 operation by ensuring businesses achieve greater compliance. In the previous year, about RM1.5 billion was collected through the CBOS 2.0 operation. RMC aims to inspect about 200,000 of the 433,000 GST registered companies in the CBOS 3.0 operation this year. As much as taxpayers who practise good GST compliance culture should not face any concerns, taxpayers who have been dodging GST or not complying with the timeline prescribed by law should come clean and make a voluntary disclosure to the RMC in order to avoid hefty sanction.

This article is reproduced, with permission, from the Legal Herald Special Issue on GST (May 2017 issue), a publication by Lee Hishammuddin Allen & Gledhill, Advocates & Solicitors, Kuala Lumpur, Malaysia