As daily news heralds the emergence of the British economy from the worst recession since the 1930s it may seem a strange time to suggest that companies should consider acquiring businesses from companies which go into an insolvency process.

However, looking back at past recessions shows that, apart from a spike of insolvencies when the recession first bites, the peak of insolvencies occurs a surprisingly long time after the economy has returned to growth. For example, the global recession is the early 1980s ended in the UK at the beginning of 1981 but the peak of company failures did not occur until 1985. Similarly, the UK economy technically emerged from a recession in the third quarter of 1991 but corporate insolvencies did not peak until the end of 1992.

Although making comparisons is dangerous because recessions are caused by different factors, it appears that the longer and deeper the recession the greater is the time lag following official recovery before the number of insolvencies begins to grow towards a peak.

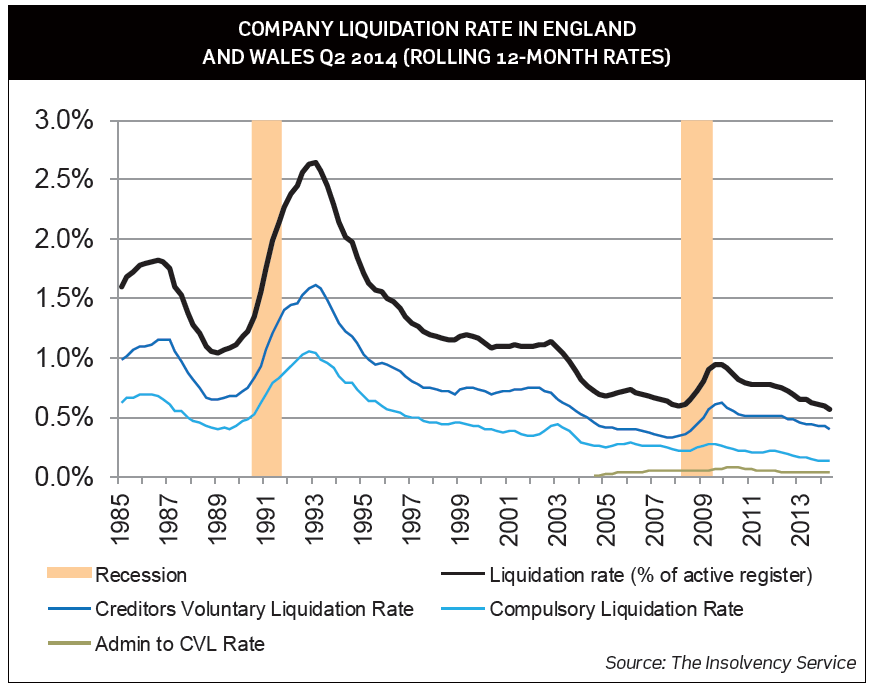

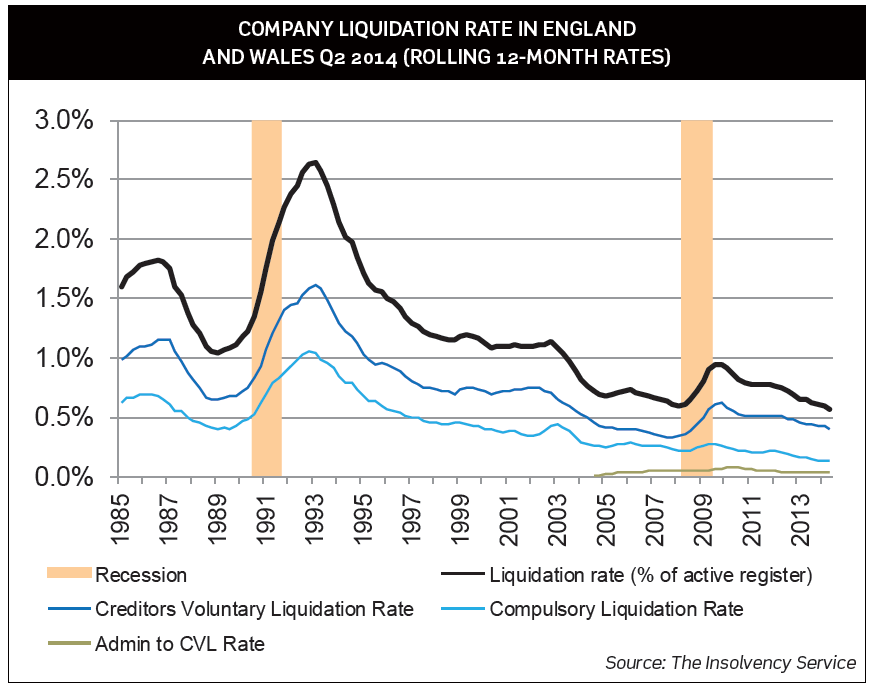

Below is a table showing the rate of company liquidations compiled by the Insolvency Service from its own statistics and the records at Companies House. The rate of company administrations will generally have a similar trajectory and it will be noted that the peak following the 1990s recession can be seen. It is notable that despite the length and depth of the last recession the trend for all sorts of liquidation are currently at historically low levels and continuing to decline. Very few people in business expect the trend to continue and experts predict that insolvency levels will rise significantly. The only question is when.

CURRENT INSOLVENCY RISKS

There are a number of factors which may contribute to a sharp rise in insolvencies. Interest rates are at historically low levels but, despite this, research by R3 (the Association of Business Recovery Professionals) paints a worrying picture should interest rates rise even to a modest degree. According to their research published in September 2014:

- 135,000 businesses are currently negotiating payment terms with their creditors (up from 74,000 in February 2013);

- 154,000 businesses are just paying interest on their debts (up from 103,000 in November 2013); and

- 100,000 businesses say they would not be able to repay their debts if there was a small rise in interest rates.

As healthy businesses begin to feel more confident and seeking opportunities to grow, banks and other creditors may feel that there may be a market for the assets of those businesses which are struggling and may be more inclined to take action rather than waive ongoing breaches.

Another risk factor for businesses which is often overlooked is that, when the economy picks up, some companies which have struggled during the recession may have insufficient working capital to support an increased order book. If customers of such businesses delay payment, such businesses may find themselves without the cash to pay their creditors and be forced into an insolvency process despite a healthier order book.

THE INSOLVENCY PROCESS

For companies looking to grow by acquisition, an understanding of the insolvency processes and the opportunities (and risks) for potential acquirers is vital.

Since the 1970s, various governments have tried (and largely failed) to introduce an insolvency regime which preserves jobs and value from insolvent businesses. The latest significant attempt was introduced by the Enterprise Act 2002 which dictated that administration would be the process to be followed where it was considered that a viable business could be preserved.

In the vast majority of cases where companies go into administration, the administrators will be seeking a purchaser for the business and assets of the company concerned. Whether the administrator continues to run the business in administration or seeks a purchaser through the so-called ‘pre-pack’ or ‘accelerated M&A’ processes (where a purchaser is sought and a deal agreed prior to the formal appointment of the administrator), speed is likely to be of the essence. Where a business goes into the process or is rumoured to be heading that way value begins to evaporate rapidly. Customers and suppliers are naturally cautious of doing business with it. Creditors will do what they can to reduce their exposure and key employees will be looking around for new jobs. In addition, administrators will generally try and complete the process as quickly as practicable to obtain value and avoid this being eroded by the costs of the administration.

Compared to a normal sale process, the opportunity to carry out due diligence is limited or non-existent and the administration sale agreement will contain virtually no representations or warranties which a purchaser would rely on in a normal sale. To reflect the increased risk, the sale price is normally significantly less than would be obtained through a conventional sale process.

Companies seeking opportunities to acquire from administrations would be wise to prepare by making sure that they have funding in place and to take over the running of the business.

TUPE FACTORS

When assessing the prospective acquisitions of a business through an administration, a significant factor is often the extent of liabilities that will come with the acquired employees. Changes have been made to the TUPE regulations (most notably in 2006) with the intention of promoting the ‘rescue culture’ by limiting the extent of such inherited employee liabilities, which were seen as a disincentive to potential acquirers. The amendments drew a distinction between ‘terminal proceedings’ and ‘non-terminal proceedings’ so that, in general terms, where a business was acquired from terminal proceedings (which would include all liquidations) employee liabilities would be left be but, in non-terminal proceedings, the automatic transfer principle still applies with some exceptions such as arrears of pay or holiday pay for holidays taken (but untaken accrued holiday entitlements transfer). Perhaps rather unhelpfully, the Court of Appeal held in Key 2 Law (Surrey) LLP v De’Antiquis [2011] that administration (including those resulting from the pre-pack process) were non-terminal proceedings. As a result, seeking to limit the extent of inherited employee liability is often a significant element in negotiations with administrators or potential administrators in a pre-pack. There is a fine line between dressing up a business to make it look more attractive to potential purchasers by shedding staff (which are likely to be unfair dismissals) and making staff redundant for necessary cost saving reasons (which are likely to be fair). An understanding of the regulations and the parameters of what will be regarded as fair and unfair dismissals may result in a substantial reduction in inherited employee liability through negotiations with the administrator. There is also a limited scope to amend the terms and conditions of employment of inherited employees to align them with the terms and conditions of the purchasing business.

ACQUISITION STRATEGIES

A good strategy to build business is to acquire the business of a struggling competitor and it is often the case that rumours circulate in an industry or business sector when a company is at risk. Picking up rumours and doing some discrete due diligence will put potential purchasers in a good position to negotiate with an administrator if they are going to be appointed. Experience shows that the following points will also help secure a successful transaction.

SIX TOP TIPS FOR BUYING FROM AN ADMINISTRATOR

- Be quick or be dead. If there are several interested parties, a buyer will stand little or no chance of success unless they are ready to do a deal very quickly. Any due diligence must be rapid and highly focused, funding must be arranged and be immediately available and the professional team briefed to negotiate and document the terms within a very short period of time. It is a good idea for prospective buyers to assemble their purchase team and have a dry run exercise so that, when a real prospect arises, everyone knows their role and are able to respond rapidly.

- Cash is king. Unless there are no other offers, administrators will generally go with the buyer who offers the most cash on the table at completion, even if deferred consideration or shares in future profits might produce a bigger figure. Unless the difference is dramatic, cash on the table will normally win.

- Don’t ask for the impossible. An administrator is a professional who is normally parachuted into the business to be sold at a late stage and, as a result, will only have a limited knowledge of what they have to sell. For these reasons, buyers should recognise that it will be a case of ‘extreme caveat emptor’ and they will be wasting their time by asking the administrators for any representations or warranties which might give protection against unforeseen liabilities.

- Talking to the management. A key element in a successful purchase is often the management team that comes with the business. Buyers should be careful to keep their discussions with the management team on the terms in which they may go with the business entirely separate from the discussions with the administrator on the purchase. Under the practice guideline for the pre-pack or accelerated M&A process, the management team should be separately represented from the administrator.

- Employee and landlord issues. Although all the ordinary debts of the company in administration will be left behind, if a buyer wishes to stay in the same premises and take on the staff, significant issues can arise in respect of unpaid wages or rent. As referred to above, recent changes in employment legislation have reduced some risks related to employees and landlords are prevented from taking any action while the company is in administration. Any deal with the landlord should be negotiated (if possible) before a sale is concluded and while the administration protection remains.

- Hit the ground running. Once a buyer has bought a business from administration, they can expect a host of claims and problems to arise in the first few days. Suppliers of goods and equipment may claim title and the return of assets. Service providers may refuse to continue supply or hold the business to ransom and customers may try and renegotiate the terms on which they do business. Be prepared and have your ‘fire-fighting team’ ready to take action.

Even a well-prepared purchaser and their team can experience some unwelcome surprises and it is wise to have a fire-fighting team on standby to deal with the unexpected.

A good example of this is provided by a recent acquisition of a substantial hotel group from administrators. The hotels had continued to trade in the administration and as a result, creditors and suppliers were prevented from taking action by the administration ‘ring fence’. As soon as the sale was completed the ring fence was lifted and the protection lost. It happened that one particular high-rise hotel in the group had completed a full refurbishment of its lift system shortly before the owning company went into administration. Soon after the sale, the duty manager was pleasantly surprised when a couple of people from the lift engineers called to ‘carry out some checks’ on the newly refurbished lifts. He was very unpleasantly surprised to be told that the lift system had completely stopped working as the ‘helpful’ lift engineers had removed the vital control cards. The lift company had not been paid for the work and the control cards were subject to retention of title. Some frantic negotiations and a substantial payment were required to enable lift functions to be restored. Future visits from suppliers were treated with extreme caution.

Buying from administration can be hugely profitable, but, as seen from the ‘war story’ above, it may also be hugely risky. Wise buyers often form a new company for the purpose of the acquisition so as to limit the downside risk if it all goes horribly wrong.

CONCLUSION

The recovery of the UK economy is welcome news to all but, paradoxically, may also create the environment when company failures increase. The upside is that, in a more buoyant economy, there will be more purchasers in the market with the result that businesses and jobs may be preserved while providing purchasers with great opportunities to grow by acquisition from administration.

By Robin Tutty, consultant, Druces LLP.

E-mail: R.Tutty@druces.com.