The government has recently announced the winners of the first auction for its non-fossil fuel Contracts for Difference (CfDs). These CfDs will ultimately replace the main existing subsidy support for renewable energy, the Renewables Obligation (RO), and are a key part of the government’s Electricity Market Reform (EMR) package. The award follows many years of consultation and development and the much talked about move to an auction system pitting technologies against each other in a bid for 15-year revenue support for projects once they have been commissioned.

Background

The first auction round for CfDs was inevitably going to be controversial for the non-fossil fuel sector. Renewables had seen nuclear being awarded £92.50 per Megawatt/hour (MW/h) for a period of 35 years and it’s fair to say there was a degree of both excitement and nervousness as to which type of renewables projects would win under the auction and at what support price. The situation was further complicated by a last-minute decision by the UK government following extensive deployment of ground mounted solar, to announce that, from the end of March 2015, large-scale solar would no longer qualify for the RO. Solar had expected to be able to rely on the RO until 2017, alongside the other renewable technologies, so this decision sent the large-scale solar sector into somewhat of a frantic rush to familiarise themselves with the whole concept of CfDs, how they might qualify for them and what bid strategies to adopt. This article addresses some of the key lessons learned from the first auction and points out some of the issues which government and the renewables sector will need to address ahead of the next auction, which is due in October.

On 26 February this year, DECC announced that 27 contracts worth £315m had been offered to projects to cover delivery of over 2 Gigawatts of renewable electricity across the UK. Contracts were awarded to 750 MW of onshore wind, 72 MW of solar photovoltaic (PV) and over 1.1 Gigawatts of offshore wind projects. The full list of projects that qualified to be offered a CfD are listed below alongside the capacity and the strike price awarded.

Prices and Budget

The fundamental basis of the CfD model is the award to the successful projects of a ‘strike price’ for all eligible electricity generation from the project for a maximum of 15 years. The agreed strike price operates against a market reference wholesale price of electricity. If this reference price is lower than the strike price awarded, the CfD counterparty will pay to the generator the difference between the two prices, whereas if the reference price is higher than the strike price awarded, the generator will have to pay the difference to the CfD counterparty. The hope and aim of the CfD is to provide the generator with a predictable and stable revenue stream for its electricity. During the development of EMR and the negotiations and the development of the CfD, government consulted on ‘administrative strike prices’ for each of the various renewables technologies. The administrative strike prices were set by government by reference to the constraints within its Levy Control Framework (LCF) (the government’s allocated spending cap) and an expectation of each of the technologies’ future costs. The whole concept of the CfD regime is aimed at delivering savings to the consumer relative to the current RO regime, which will ultimately be phased out in 2017.

It was initially envisaged that CfDs would be allocated on a first-come, first-served basis, but it was always the intention of government to eventually have technologies competing on an auction basis to achieve CfD support. This acts as a driver to force down prices and to reward the lowest cost deliverable technologies with support. As the CfD concept developed, the government’s view on when to impose auctioning changed. This was partly because of the growing amount of renewable deployment in recent years and also as a result of EU rules around state aid. Fairly late in the day the government announced that the LCF budget reserved for the CfD auction would be divided between a group of ‘established technologies’ (onshore wind and solar) and ‘less established technologies’ (including offshore wind, wave and tidal and advanced conversion technologies). Auctions would apply from the outset in the established technology group, throwing for example solar and onshore wind into competition with each other and if there were more projects than auction budget in the less established technology group those projects would also compete, subject to a few rare exceptions.

The one potential upside for auction participants is the ‘pay as cleared’ system. Under this system, CfD auction bids are ranked from lowest to highest £MW/h bid. The lowest bids in each technology grouping (established and less established) are awarded a CfD until the budget for the technology grouping is used up. This allocation and budgeting process takes into account that, under the auction rules, each successful bidder has its strike price increased to be equal to the strike price of the most expensive successful bidder in that delivery year or the successful bidder’s administrative strike price, if lower.

The budget allocation for the first CfD auction, despite last minute alteration, was low in comparison to the amount of support available to RO projects. The practical effect of this was to effectively ensure there would be auctions across the two technology groupings, resulting in fierce competition and some big losers.

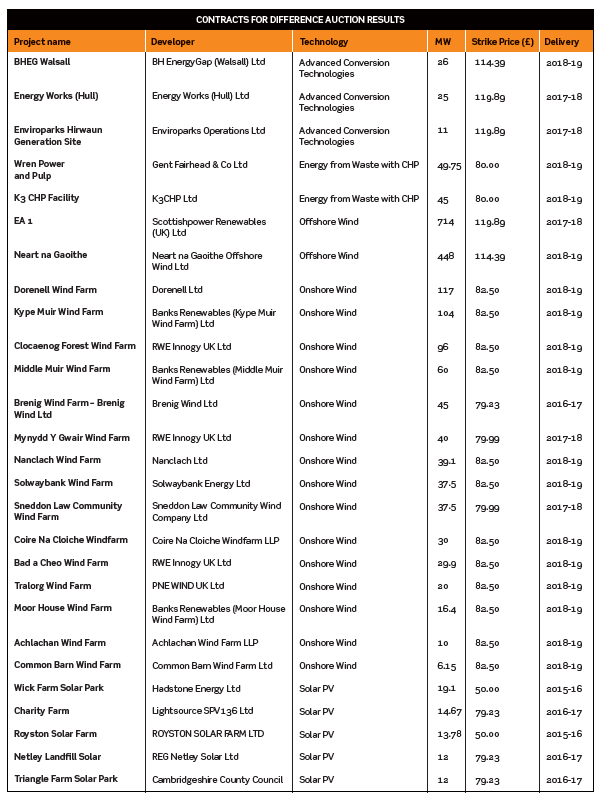

The effect that this competition has had on the prices achieved by the technologies compared to the original administrative strike prices proposed by the government is apparent from the award announcement.

Solar, for example, had an administrative strike price of £120 per MW/h. You can see from the table above that the two successful projects for the delivery year 2015/16 achieved a strike price of £50 per MW/h. Similarly, onshore wind, with a strike price of £95 MW/h, achieved in the case of the Brenig Wind Farm, £79.23 MW/h.

Lesson one

There is a very real allocation risk for developers and projects. Competition is fierce. This system must, and does, favour the bigger developers, who are generally more able to carry the cost of developing a project up to the point of planning and grid in order to qualify to bid in a CfD auction and live with the risk of being unsuccessful. State aid rules at an EU level mean that auctions are here to stay.

Lesson two

The budget set for the first allocation was low. That is perhaps understandable given it was in effect a ‘trial run’ but there were some big losers. Government will hail the auction as a success as it demonstrates competition and takes the renewables sector away from the mentality that had developed that, if you build your project, you automatically get subsidy support. The LCF budget available is £7.6bn to 2020. However, this amount needs to support, among other things, nuclear, which has not been put to auction, the RO and Feed-in Tariff (FiT) and legacy RO and FiT projects entitled to continuing support. It has quickly become clear that the LCF is inadequate and could act as a brake on deployment of clean energy at a time when the costs of many of these technologies are coming down and industry critical mass is needed to preserve the UK’s important position in this market (and the jobs associated with that). To compound the issue, there is as yet no budget allocated beyond 2020, so no clear support signal which those major projects with significant timelines can plan for. If the government can sort this out, it will go a long way to bolstering confidence in the sector.

The prices achieved in the auction by the successful applicants have been subject to much comment since the announcement. The two solar projects which achieved £50 MW/h will not be built out because they are simply uneconomical at that level. There is also a great deal of concern as to whether a number of the other projects will ever be built at the CfD strike price awarded. The low prices bid compared to the administrative strike price will be used by government to demonstrate that this new support system can drive down costs and will be described as a success. But it is only a success if the projects get built and one only has to look at the old NFFO contracts and auctions back in the 90s to demonstrate this point. It is true, however, that the CfD auction has concentrated the industry’s mind on driving down the cost of renewables, which needed to happen. One of the most likely areas of cost efficiencies will be through falling equipment prices, (the cost of turbines, panels and plant). While the supply chain won’t like this, it is something that will need to happen for renewables to continue to achieve public support and compare favourably in a cost constrained, post-recessionary world, against conventional fossil fuelled power.

Lesson three

Tactical bidding doesn’t necessarily work. There is certainly a strong sense that a number of developers were looking to bid low and benefit from a strike price uplift from the ‘pay as clear’ system in the auction to ensure they obtained a CfD at a deliverable strike price. The industry may not thank them for that and neither should government if ultimately the projects do not go ahead.

Auction rules

It was not until we approached the first allocation round that it became clear that auctions were inevitable. DECC was issuing and amending auction rules right up to the last minute. There is no doubt that this left some developers in great difficulty, particularly those in the solar sector who had not expected to have to bid for CfDs initially but found they had to with the late announcement that the RO would not be available to them post end March 2015.

Lesson four

Going forward, the lessons to learn from this process for all parties involved are:

- The need for greater dissemination of information and explanation around auction rules and proper, understandable and simplified guidance from DECC, such that late entrants into the sector can still bid for CfDs;

- Those in non-fossil fuel development and their advisers should spend time becoming familiar with the auction rules and learning from the first results, as well as working through bid tactics;

Auction Eligibility

For each allocation round, there is essentially a pre-qualification process to ensure that a project is eligible to bid for a CfD. This involves providing certain evidence (eg planning permission and grid connection evidence) and filling in the application form. Applicants are notified as to whether they have passed this stage and, for unsuccessful applicants, there is then an appeal mechanism. The importance of this stage cannot be underestimated. If a project is kicked out at this stage, it will have to wait until the next allocation round and in some cases that will mean the project may never go ahead.

Lesson five

The pre-qualification process is crucial. A number of developers/projects were unsuccessful at this stage. A lesson for developers is to be rigorous in filling in forms and providing relevant information. Simple mistakes result in rejection and lead you down the uncertain process of appealing the decision. For government, the lesson is have a process that does not lead to clear and obvious errors disqualifying projects when it is clear that they are minor errors, as this just leads to further cost and time for all participants and delays to the allocation process. If an appeal is necessary, legal input and a properly structured case and arguments can be crucial as those developers who successfully appealed will no doubt testify.

Features of the Auction

Once eligibility is determined, CfD allocation occurs. Assuming that there is insufficient budget to allocate CfDs to all projects (as was the case in the first allocation round and will inevitably be the case for future rounds) the auction principles kick in.

Key features of the auction are:

- a budget is allocated for all of the delivery years covered by the LCF. So 2015/16, 2016/17, 2017, 2018 and 2018/19;

- the clearing price for each delivery year is set at the strike price bid of the last accepted (marginal) bid in that year;

- the strike price offered to successful applicants will be the lower of the clearing price for the relevant delivery year and the administrative strike price;

- it is a sealed bid auction with strict timescales;

- developers can submit ‘flexible bids’ which allows a bidder to vary the capacity, price or delivery date of their project from the original application but the flexible bid with the lowest strike price will always be considered first;

- projects compete across all delivery years and technologies, so, for example, a lower strike price bid for a project intended to be commissioned in 2017/18 will beat a similar project with a higher strike price bid in 2015/16;

- the published budget covering the delivery years is not cumulative. This can lead to some bizarre situations such as a project for delivery in 2018/19 taking most of the budget pot because it is cheaper than other projects for delivery in 2015/16 etc. Take for example the successful solar projects in this auction round. Those that were awarded £79.23 for delivery in 2016/17 will have bid lower than other non-successful solar and onshore wind projects in the same ‘established technology group’ in 2015/16.

Lesson six

The auction is not about delivery as early as possible but rather about the least cost delivery and, if that means that nothing gets built until 2018/19, so be it. Developers need to understand that and government need to realise that this is inevitably going to drive an even greater push to commission projects under the RO (although time is running out for this), which in turn will limit the share of the LCF that CfDs can access.

Signing and Conditions Precedent

Once an applicant has been notified of success in the auction, there are strict timetables to adhere to and instructions from the Low Carbon Contracts Company (the CfD counterparty) to follow. The deadline for signing the first CfDs has passed and initial conditions precedent in the CfD should have been fulfilled, including the provision legal opinions.

Lesson seven

The CfD is made up of the front end CfD agreement and back end standard terms and conditions. It is a large document running to over 500 pages and it is essential that an applicant understands the obligations it is entering into ahead of the auction. Applicants should make sure they are prepared in advance to fulfil the initial conditions precedent, otherwise the timing deadlines become very tight. The CfD contains some ongoing key deadlines and milestone dates which do not allow projects to drift. Success in the auction is therefore only the start.

Lesson eight

The CfD process and first auction has demonstrated that CfDs do not work for smaller nascent technologies. The CfD was never designed to incentivise these small-scale projects and some of them can qualify under the small-scale FiT. However, the marine energy sector in particular, has recognised that demonstration plants and marine test facilities will need to lobby for a modified regime or access to the FiT (which they do not currently have).

Lesson nine

Aside from the large-scale solar sector there was still a sense among many developers that they can still access the RO and build out under it to 2017. That may have led to many deciding not to choose to bid in the first CfD auction. However, as the construction window to commission a project by the end of March 2017 narrows we are likely to see many more participating in the forthcoming auctions leading to even greater competition.

Conclusion

Government has seen the first CfD auction as a success. Although consultation has already begun on tweaking the regime in readiness for the next auction in October this year, it is unlikely there will be fundamental changes. The first auction has provoked concern in the renewables sector. However, time and a settled regime which is better understood can allay those fears. The key areas for government to address and for the industry to lobby on are the budgets available for forthcoming auctions and clarity on budgets post 2020.